-

tel:

+86-18961602506 -

email:

fly03@flynewenergy.com

FLY

GGII: Top ten predictions for China’s lithium battery industry in 2024

Dec 29, 2023

The Advanced Industrial Research Institute (GGII) has made ten predictions for China's lithium battery market in 2024. Among them, GGII predicts that China's lithium battery market shipments will exceed 1,100GWh in 2024, a year-on-year increase of more than 27%, officially entering the TWh era. Among them, power battery shipments exceeded 820GWh, a year-on-year increase of more than 20%; energy storage battery shipments exceeded 200GWh, a year-on-year increase of more than 25%; it is expected that in 2024, China's four major lithium battery materials shipments will grow by more than 20%. Among them, cathode material shipments exceeded 3 million tons, lithium battery separator shipments exceeded 22 billion square meters, anode material shipments exceeded 2 million tons, and electrolyte shipments exceeded 1.3 million tons.

GGII pointed out that after the rapid expansion of the lithium battery industry chain from 2020 to 2022, the market will gradually show "fatigue" in 2023. Market weakness is mainly reflected in three aspects: a significant reduction in new bidding projects, a low completion rate of corporate goals, and product prices cut in half.

From the perspective of new bidding projects, GGII survey data shows that the bidding volume of the entire lithium battery industry chain in 2023 will drop by about 50% compared with 2022.

Judging from the completion of scheduled goals, combined with public information, except for a few companies, the goals set by main engine manufacturers and battery factories at the beginning of 2023 have not been achieved. Companies with better production and sales can complete more than 60% of the goals set at the beginning of the year. Most companies The completion rate is 40-55%. Among them, some third-tier and below-tier companies have begun to experience operational difficulties due to issues such as overcapacity, lack of customers, and cost disadvantages.

From the perspective of product prices, product prices in all links of the industrial chain have halved compared with the beginning of the year, and materials such as lithium salts have even dropped by more than 70%, resulting in a significant decline in the profitability of industrial chain companies. The original "prosperous days" (gross profit margin 25-40%) It has become "cold and freezing" (gross profit margin 15-20%), and it is expected that the "pain" caused by falling prices will continue in 2024.

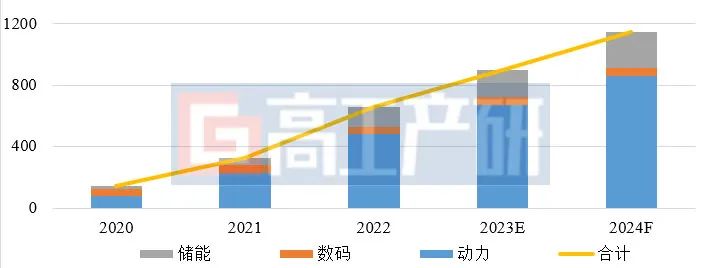

1. China’s lithium battery shipments exceeded TWh for the first time, and the power and energy storage lithium battery market grew by more than 25%

In 2024, China's lithium battery market shipments will exceed 1,100GWh, a year-on-year increase of over 27%, officially entering the TWh era. Among them, power battery shipments exceeded 820GWh, a year-on-year increase of more than 20%; energy storage battery shipments exceeded 200GWh, a year-on-year increase of more than 25%.

China’s lithium battery shipments and forecasts from 2020 to 2024 (GWh)

Source: Advanced Industrial Research Institute (GGII), December 2023

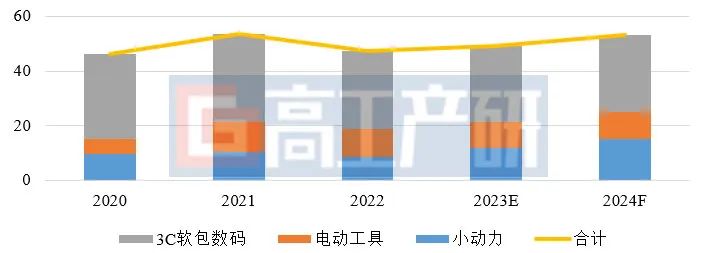

2. China’s digital battery shipments exceeded 50GWh, with growth coming from the small power market

The downturn in the global economic environment has led to a decline in growth in areas such as infrastructure, steel, real estate, and large consumption. It has been unable to drive consumer products (such as power tools, mobile phones, tablets, and laptops), thereby reducing the demand for lithium batteries.

GGII expects China’s digital battery shipments to exceed 50GWh in 2024, a year-on-year growth of over 3%. Among them, the shipment volume of 3C soft-pack digital batteries and lithium batteries for power tools increased by 1-2%; the demand for lithium batteries in markets such as port machinery and AGV is expected to grow by more than 5%; benefiting from the decline in product prices, lithium batteries for small power use The market will achieve growth of more than 15%.

China’s digital lithium battery shipments and forecast (GWh) from 2020 to 2024

Source: Advanced Industrial Research Institute (GGII), December 2023

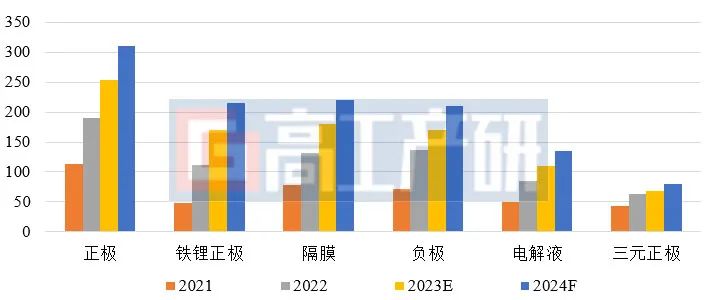

3. The year-on-year growth rate of shipments of the four major main materials all exceeded 20%.

GGII predicts that in 2024, China's shipments of the four main materials for lithium batteries will all grow by more than 20%, of which cathode material shipments will exceed 3 million tons, lithium battery separator shipments will exceed 22 billion square meters, and anode material shipments will exceed 2 million tons. , electrolyte shipments exceeded 1.3 million tons.

Shipment volume and forecast of main materials in China's industrial chain from 2021 to 2024 (10,000 tons, 100 million square meters)

Source: Advanced Industrial Research Institute (GGII), December 2023

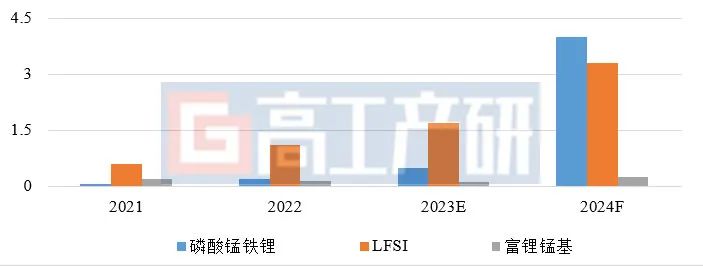

From the perspective of the main product structure, lithium iron phosphate cathode materials account for nearly 70% of the total cathode material shipments, and ternary cathode materials account for less than 26%; the lithium iron manganese phosphate material market shipments will exceed 30,000 tons, year-on-year An increase of over 500%. Driven by the growth in demand for lithium manganate materials, China's shipments of lithium-rich manganese-based materials will increase by more than 50% (mainly used for doping).

Driven by the growth of lithium iron phosphate batteries, China's LiFSI market demand will exceed 30,000 tons in 2024, with the market growth rate exceeding 100%. In 2024, domestic shipments of lithium replenishing materials such as lithium ferrite will grow by more than 30% (for use in phosphate batteries).

Double-layer coating technology has limited impact on natural graphite shipments. Artificial graphite accounts for more than 86% of the total shipments of the anode material market. Driven by the "1-10" increase in power large cylindrical batteries, the silicon-based anode material market will be in 2024. The cargo volume will exceed 35,000 tons, a year-on-year increase of over 80%.

Segmented cathode material shipments and forecasts from 2021 to 2024 (10,000 tons)

Source: Advanced Industrial Research Institute (GGII), December 2023

4. The domestic lithium battery industry chain welcomes the "year of implementation" of overseas layout, with Southeast Asia, Eastern Europe and South America being the main areas of implementation.

2023 is the year when domestic lithium battery industry chain companies will focus on going overseas. More than 20 companies (lithium battery companies, cathode companies, equipment companies, etc.) have investigated in Southeast Asia, Africa, Eastern Europe and South America (including Central America), but few companies have actually implemented it, and they are still in the early stage of market research. As competition in the domestic market intensifies, GGII predicts that 2024 will be the "year of landing" for domestic lithium battery industry chain companies overseas, with Southeast Asia, Eastern Europe and South America (including Central America) becoming the main areas for project landing.

Source: Advanced Industrial Research Institute (GGII), December 2023

5. Large cylindrical batteries and (semi-) solid-state batteries for power use will welcome the "1-10" phased increase in volume

In the field of new energy passenger vehicles, domestic (semi-) solid-state battery shipments will exceed GWh in 2023. Combined with the planning of leading OEMs, GGII predicts that more than 5 new models equipped with (semi-) solid-state batteries will be put on sale in China in 2024. It is expected that the shipment volume of (semi-) solid-state batteries in 2024 can achieve 5GWh level shipments.

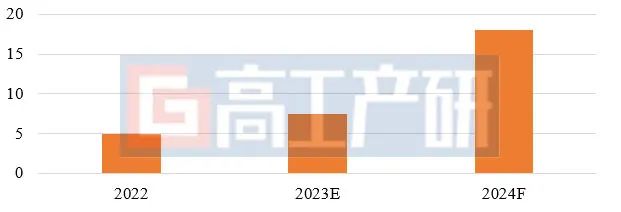

In terms of large cylindrical batteries for power, currently large cylindrical batteries with multi-lugs aluminum shells (3/4/6 series) have been shipped in batches, and large cylindrical batteries with all-lugs steel shells for power have completed the transition from "0-1" Mass production breakthrough, it is expected to usher in GWh-level batch deliveries in the passenger car field in 2024, opening a new stage of "1-10".

Domestic large cylindrical battery shipments and forecasts from 2022 to 2024 (GWh)

Source: Advanced Industrial Research Institute (GGII), December 2023

6. Fast-charging lithium batteries meet the "quantity + quality" breakthrough, and the product rate performance moves from 1.3-1.7C to 1.7-2.5C

The field of 3C soft pack digital batteries has achieved fast charging capabilities above 4C and is widely used in the consumer market. At present, more than 10 domestic power battery companies have deployed fast charging technology. The current mainstream rate performance is concentrated at 1.3-1.7C. In 2024, the average rate performance of the domestic power battery market will exceed 1.7C and gradually move towards 1.7-2.5C.

It is expected that there will be more than 15 new fast-charging models (average charging rate greater than 2C) launched in China in 2024, and China's fast-charging model shipments are expected to exceed 50,000 units. Combined with the concentrated release of new models on the 800V platform from overseas OEMs, it will drive domestic shipments of fast-charging lithium battery products to exceed 10GWh.

Driven by fast-charging lithium batteries, China's shipments of materials such as oligo-wall (or double-wall, single-wall) carbon nanotubes, fast-charging electrolytes, small particle size cathode materials, and new lithium salt additives will exceed 80% in 2024 increase.

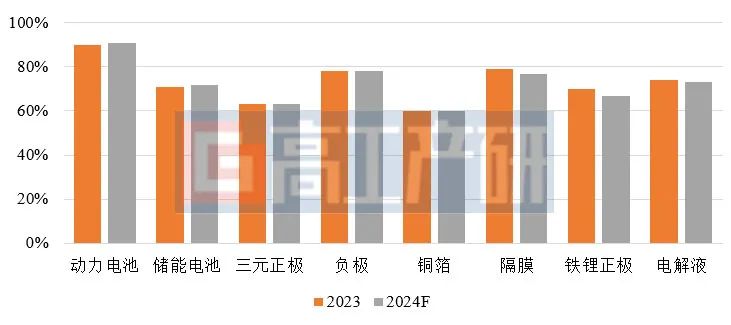

7. The CR5 concentration of the power/energy storage battery increases by 1~2 points, and the CR6 concentration of the separator/lithium iron cathode/electrolyte decreases by 2~4 points.

From the perspective of market concentration, in the battery field, China's power battery and energy storage battery market CR5 concentration in 2024 will still show an upward trend compared with 2023. The CR5 concentration rate in the power battery market will exceed 90%, and the CR5 concentration rate in the energy storage battery market will exceed 72%.

In terms of materials, the CR6 concentration ratio of China's lithium battery copper foil, negative electrode and ternary cathode market in 2024 will be the same as in 2023 (60%, 78% and 53% respectively in 2023). The concentration of separators, lithium iron cathodes and electrolyte CR6 will drop by another 2-4 percentage points based on 2023 (77%, 67%, and 73% respectively in 2023).

Changes in concentration in some fields from 2023 to 2024 (%)

Note: The power battery and energy storage battery adopt the CR5 format, and the main battery material adopts the CR6 format.

Source: Advanced Industrial Research Institute (GGII), December 2023

8. The price of products in the main links of the lithium battery industry chain has dropped by 5~15%, driving the cost of lithium batteries down by 0.03-0.06 yuan/Wh.

In 2024, the prices of products in the main links of the lithium battery industry chain will be reduced by 5% to 15% based on 2023. Among them, the negative electrode, electrolyte and other links dropped by 5~12%, and the positive electrode, separator and other links dropped by 8~15%. In addition to materials, the prices of lithium battery production equipment and related parts will also continue to decline in 2024 based on 2023.

The falling prices of raw materials and components have led to a 5-10% drop in battery costs, and the cost of lithium batteries will drop by another 0.03-0.06 yuan/Wh on the current basis.

Source: Advanced Industrial Research Institute (GGII), December 2023

9. The negative electrode of petroleum coke medium-high sulfur coke system is expected to achieve a "0-1" breakthrough, and the "tightening" of the battery assembly line will gradually be "unblocked"

In terms of raw material cost reduction, the proportion of low-cost raw material applications will continue to increase. For example, high-sulfur coke for negative electrodes is expected to achieve a "volume" breakthrough in 2024, enabling small-scale batch shipments, driving the cost of finished negative electrode products down by 5-10%; ultra-thin copper foil and composite current collectors of 4.5 μm and below are difficult to achieve in the short term. 10GWh scale scale expansion. 6μm lithium battery copper foil is still the mainstream cost-effective current collector material; in terms of upstream raw material discounts, compared with the 92~94 discount for nickel/lithium in 2023, the nickel/cobalt/lithium salt pricing coefficient in 2024 is expected to achieve a 90% discount across the board.

In terms of production line efficiency, the average production efficiency of square battery assembly lines will move towards 30-35PPM (22~28PPM in 2023), and the production efficiency of 46 series steel-cased large cylindrical battery assembly lines is expected to achieve a breakthrough of 100~150PPM (2023 is 50~100PPM).

10. The production capacity utilization rate in each link is less than 60%, ineffective production capacity is being cleared at an accelerated pace, and equipment companies are now facing a survival crisis.

From the perspective of production capacity utilization, the effective production capacity utilization rate of the domestic power battery market in 2024 (excluding ineffective production capacity that has not been started and has not passed downstream verification) will be less than 60%, and the effective production capacity utilization rate of the energy storage battery market will be less than 50%. Most new companies have released newly released production capacity into ineffective or inefficient production capacity.

In 2024, the anode material industry's production capacity will exceed 4.5 million tons, separator production capacity will exceed 32 billion square meters, ternary cathode material production capacity will exceed 2 million tons, and lithium iron phosphate cathode material production capacity will exceed 5.5 million tons. Except for diaphragms, the capacity utilization rate of other main materials is less than 45%, and the top 4~8 companies in the industry share more than 90% of the market share.

From the perspective of equipment bidding, the new bidding capacity of domestic power and energy storage batteries will be less than 250GWh in 2024, and the directly corresponding new equipment market size will be less than 70 billion. The equipment market will be difficult to reproduce the peak of the industry scale in 2022.

China's lithium battery market bidding capacity from 2022 to 2024 (GWh)

Source: Advanced Industrial Research Institute (GGII), December 2023

In 2022, the domestic lithium battery production equipment bidding volume will mainly be concentrated in first-tier/second-tier battery companies, with the bidding volume accounting for more than 80% of the total. Entering 2023, most of the bidding projects of first-tier battery companies are in a state of delay, while energy storage battery companies/large cylindrical battery companies/second-tier battery factories and OEM self-built battery factories have opened bidding. The combined demand of these companies accounts for more than 1% of the new equipment market. 85%.

Due to fierce competition in the main field of production equipment, some equipment companies need to develop new business growth and profit points. According to incomplete statistics from GGII, the number of companies that will flock to the segmented track from 2022 to 2023 exceeds 80. Behind the explosive influx is fierce competition and fierce "fighting." In 2024, the survival crisis faced by equipment companies will be even more severe.

Number of lithium battery equipment companies (houses) that have lithium battery machine vision inspection systems, lithium battery CT equipment, photovoltaics, and magnetic levitation transportation systems

Recent Posts

Contact US

Product Information

Quantity

Unit

Piece

Support order samples, customization, wholesale direct, and complete payment. If the product you look for does not have corresponding customized content, pls fill out the form below to contact us, and we will reply ASAP.